Ceiling Fans Market Overview - Definition, scope, and significance?

The ceiling fans market encompasses the design, manufacture, distribution, and installation of ceiling-mounted rotary fans used for air circulation and cooling in residential, commercial, and industrial spaces. Its scope covers a wide range of product types, including standard, energy‑efficient, smart‑connected, and decorative fans, as well as related accessories and services. The market is significant because ceiling fans provide a low‑cost, energy‑saving alternative to air‑conditioning, support sustainability goals, and drive interior décor trends worldwide.

Ceiling Fans Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising electricity costs, increasing emphasis on green building practices, and growing urbanization that fuels demand for affordable climate‑control solutions. Opportunities arise from advances in IoT integration, development of bladeless and whisper‑quiet technologies, and expanding construction activities in emerging economies. Restraints involve seasonal demand fluctuations, competition from portable air‑conditioners, and higher upfront costs for premium smart fans. Challenges stem from strict safety regulations, supply‑chain disruptions, and the need for skilled installation personnel.

Ceiling Fans Market Growth Trends - Current and emerging trends shaping the market?

Current trends feature a shift toward energy‑efficient DC motors, which reduce power consumption by up to 70% compared with conventional AC models. Smart ceiling fans equipped with Wi‑Fi, voice control, and sensor‑based speed adjustment are gaining traction in connected homes. Aesthetic customization, such as interchangeable blades and designer finishes, is influencing consumer preference. In emerging markets, affordable compact fans are driving volume growth, while premium markets see increasing demand for LED‑integrated and bladeless designs.

COVID-19 Impact on the Ceiling Fans Market - Pandemic effects and recovery trajectory?

The pandemic initially disrupted manufacturing and logistics, leading to short‑term inventory shortages. However, lockdowns heightened the need for comfortable indoor environments, prompting a rebound in residential demand for cooling solutions. Post‑pandemic, the market has exhibited a robust recovery, supported by renewed construction activity and a consumer shift toward energy‑saving home upgrades. This recovery aligns with the projected compound annual growth rate of 6.74% through 2032.

Ceiling Fans Market Competitive Landscape - Major competitors and market consolidation?

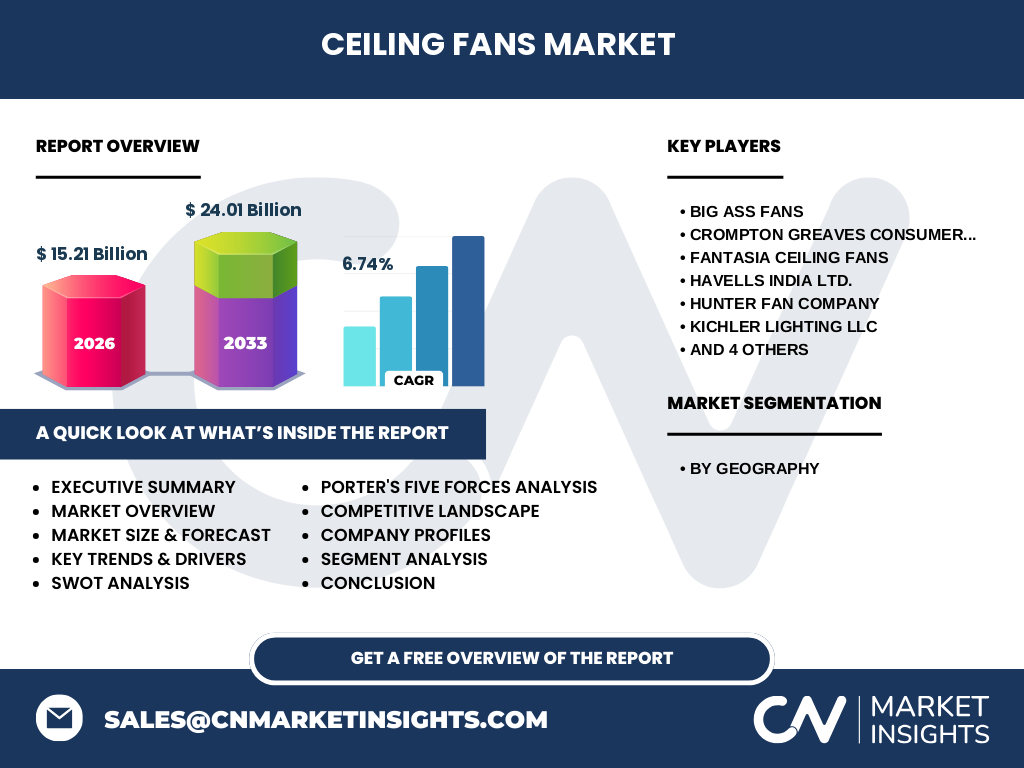

The competitive landscape is defined by a mix of global manufacturers and regional specialists. Leading players such as Big Ass Fans, Crompton Greaves Consumer Electricals, Fantasia Ceiling Fans, Havells India, and Hunter Fan Company dominate through extensive product portfolios and strong distribution channels. Recent consolidation activities include strategic acquisitions and joint ventures aimed at expanding geographic reach and technology capabilities, intensifying competition especially in the smart‑fan segment.

Executive Summary - High-level overview and key findings about Ceiling Fans Market?

The ceiling fans market is valued at $15.21 billion in 2026 and is forecast to reach $24.01 billion by 2033, reflecting a CAGR of 6.74%. Growth is propelled by energy‑efficiency mandates, smart‑home adoption, and expanding construction activities across all regions. North America and Asia Pacific present the highest demand, while Europe shows strong preference for premium, design‑focused fans. Key opportunities lie in IoT integration and sustainable motor technologies, whereas seasonal demand and regulatory compliance remain challenges.

Ceiling Fans Market Forecast - Projections for 2025-2032 period?

Based on current momentum, the market is expected to continue expanding at a steady pace, moving from the 2026 baseline of $15.21 billion to the 2033 forecast of $24.01 billion. The projected CAGR of 6.74% suggests consistent yearly growth, driven by increasing construction outputs, rising consumer awareness of energy savings, and ongoing innovation in smart and eco‑friendly fan solutions. Manufacturers that invest in digital connectivity and localized production are likely to capture the most share.

Ceiling Fans Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by geography highlights five key regions: North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America. Each region contributes to the overall market size, with North America and Asia Pacific leading due to extensive residential and commercial construction. Product‑type segmentation includes standard AC motor fans, energy‑efficient DC motor fans, and smart‑connected fans, while application segmentation covers residential, commercial, and industrial use cases.

Global Ceiling Fans Market Size and Share by Region - Geographic distribution?

Geographically, the market is distributed across North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America. North America holds a significant share thanks to high disposable incomes and strong renovation activities. Asia Pacific shows rapid growth driven by expanding middle‑class populations and urban housing projects. Europe maintains a stable share focused on premium design and energy‑efficiency standards. Emerging regions in the Middle East, Africa, and South & Central America present untapped potential for future expansion.

Regional Analysis of the Ceiling Fans Market - Detailed regional market performance?

In North America, demand is fueled by smart‑home integration and retrofitting older homes with energy‑saving fans. Europe’s market is characterized by stringent eco‑design regulations, prompting manufacturers to launch low‑power DC models. Asia Pacific benefits from large‑scale housing developments and increasing awareness of sustainable cooling. The Middle East & Africa experience seasonal spikes due to hot climates, while South & Central America see growth aligned with infrastructure investments and rising urbanization.

Leading Company Profiles in the Ceiling Fans Market - Industry players and strategies?

Big Ass Fans focuses on industrial‑grade, high‑airflow solutions and leverages strong OEM relationships. Crompton Greaves emphasizes affordable, energy‑efficient fans for the Indian subcontinent and expands via rural distribution networks. Fantasia Ceiling Fans targets the North American residential segment with design‑centric products. Havells India combines competitive pricing with extensive after‑sales service. Hunter Fan Company differentiates through premium branding and integrated lighting. Panasonic leverages its electronics expertise to embed smart controls, while Westinghouse emphasizes durability for commercial applications.

Porter's Five Forces Analysis of the Ceiling Fans Market - Competitive forces assessment?

Threat of new entrants is moderate; entry barriers include capital investment in manufacturing and brand establishment. Bargaining power of suppliers is low to moderate, as components such as motors and electronics are sourced from multiple vendors. Bargaining power of buyers is high, given the availability of numerous alternatives and price sensitivity. Threat of substitutes includes portable air‑conditioners and HVAC upgrades, which pressure margins. Industry rivalry is intense, driven by product innovation, price competition, and regional market share battles.

SWOT Analysis of the Ceiling Fans Market - Strengths, weaknesses, opportunities, threats?

Strengths: Energy efficiency, low operating cost, and wide applicability across sectors. Weaknesses: Seasonal demand cycles and dependence on construction activity. Opportunities: Smart‑fan integration, adoption of DC motor technology, and expansion in emerging markets. Threats: Regulatory changes, competition from alternative cooling systems, and supply‑chain volatility.

Ceiling Fans Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw material suppliers (steel, aluminum, plastics, electronics), proceeds to component manufacturers (motors, blades, controls), then to assembly facilities where fans are built and tested. Distribution channels include wholesale distributors, specialty retailers, and e‑commerce platforms. After‑sales services, such as installation, maintenance, and warranty support, complete the chain. Digital platforms are increasingly influencing direct‑to‑consumer sales and data‑driven product development.

Key Investment Insights in the Ceiling Fans Market - Strategic investment recommendations?

Investors should focus on companies that demonstrate strong R&D pipelines for DC and IoT‑enabled fans, as these technologies align with sustainability trends. Acquisitions of regional distributors can accelerate market penetration in high‑growth areas like Asia Pacific. Partnerships with smart‑home ecosystem providers enhance product appeal in connected‑home segments. Allocating capital toward scalable manufacturing in proximity to key demand centers can mitigate logistics risks and improve margins.

Ceiling Fans Market Conclusion - Summary and key takeaways?

The ceiling fans market is poised for robust growth, moving from a 2026 valuation of $15.21 billion to $24.01 billion by 2033 with a 6.74% CAGR. Energy efficiency, smart technology, and expanding construction activities are the primary catalysts. While seasonal demand and regulatory compliance present challenges, opportunities in IoT integration and emerging markets offer substantial upside. Stakeholders who prioritize innovation, regional expansion, and strategic partnerships are likely to achieve competitive advantage.

Research Methodology - How this research was conducted?

The study employed a mixed‑method approach combining primary interviews with industry experts, secondary data extraction from company reports, trade publications, and reputable databases. Market sizing utilized a top‑down technique anchored on the provided 2026 market size and forecast figures. Trend analysis incorporated technology adoption curves and construction activity forecasts, while competitive mapping drew from public financial disclosures and press releases.

Research Scope - Coverage and limitations?

The research covers global ceiling fan manufacturers, product categories, and end‑use applications across the five defined geographic regions. It includes quantitative forecasts through 2033 and qualitative assessments of technology and regulatory trends. Limitations are confined to the reliance on publicly available data and the exclusion of confidential corporate financials beyond the supplied market size and growth metrics.

Key Companies and Recent Developments in the Ceiling Fans Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Big Ass Fans announced a new line of ultra‑quiet industrial fans with integrated IoT sensors for predictive maintenance. Crompton Greaves launched a budget‑friendly DC motor fan series targeting rural India. Fantasia Ceiling Fans introduced a designer collection featuring interchangeable blade finishes. Havells India unveiled a smart fan compatible with major voice assistants. Hunter Fan Company released a premium LED‑integrated ceiling fan for upscale residential projects. Panasonic expanded its smart‑home portfolio with a Wi‑Fi‑enabled fan that syncs with its home automation ecosystem. Westinghouse announced a partnership with a commercial HVAC provider to bundle fans with energy‑management services.